Israel Economy War Costs GDP Contraction Debt Deficit Tech Resilience

SPOTLIGHT: ISRAEL’S ECONOMY SLIPS BACK INTO CONTRACTION AS ANNUALIZED FIRST-QUARTER GDP DROPS 3.3 PERCENT; NATIONAL DEBT RATIO SURGES TO 69 PERCENT ON MOUNTING MILITARY EXPENSES; HIGH-TECH SECTOR HOLDS GROUND AMID WORKFORCE SHORTAGES.

WarsWW Strategic Spotlight: The Cost of Total Attrition—How a Multi-Theater War Restructured the Israeli Economy

Strategic Status: WAR ECONOMY TRANSLATION / MACROECONOMIC RESTRUCTURING / DEBT PATH ACCELERATION

Theater Focus: Domestic Fiscal Resilience vs. Systemic Defense Expenditure Overload

The transformation of regional friction into an open, multi-theater campaign has fundamentally altered the structural foundations of the Israeli market. Since the initial outbreak of high-intensity operations along the northern border, the state has transitioned from an innovation-driven advanced market into a permanently mobilized war economy.

While individual tech sectors continue to display notable flexibility, the cumulative weight of extended troop mobilizations, severed trade routes, and open-ended procurement cycles has pushed public finances onto a highly precarious trajectory.

I. The Macroeconomic Trajectory: From Coiled Spring to First-Quarter Contraction

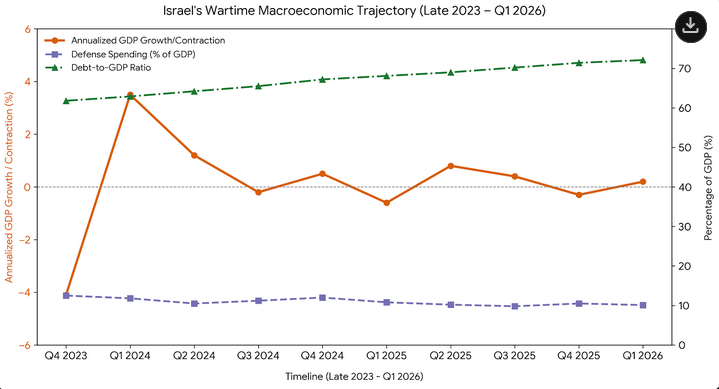

The macroeconomic footprint of the multi-front conflict is defined by severe volatility, with national output responding directly to sudden shifts in the active combat zones. Following the initial shockwaves of late 2023, which triggered an annualized 19.4% contraction in gross domestic product, the economy experienced a brief series of uneven bounces throughout 2024 and 2025.

| Operational Phase | Q4 2023 Outbreak | Full Year 2025 Base | Q1 2026 Iran Theater |

| Tactical Timeline | Initial shock following conflict outbreak | Fragile stabilizing baseline | Strategic slip during multi-front escalation |

| Macro Performance | -19.4% Initial GDP Shock | +2.9% GDP Expansion | -3.3% GDP Contraction |

| Primary Economic Vector | Comprehensive mobilization labor freeze | Speculative ceasefire trading peaks | Widespread consumer demand drop |

However, the expansion of active combat into a direct, multi-front war involving regional ballistic exchanges has effectively halted that recovery. Fresh national accounts verification data indicates that Israel’s economy contracted at an annualized rate of 3.3% in the first quarter of 2026, completely reversing the fragile gains managed during the final months of the previous year.

This downturn was felt across almost all sectors of domestic demand. Private consumer spending dropped by 4.7% as security restrictions limited commercial operations, while localized government consumption pulled back by 4.8%.

The primary driver of this economic contraction was the ongoing mobilization of reserve forces, which has kept hundreds of thousands of high-productivity workers away from their civilian roles, depressed tourism revenues, and caused intermittent school and business closures across the country.

II. The Financial Burden: Deep Deficits and the Vanishing Peace Dividend

Beyond fluctuating quarterly growth rates, the most significant long-term consequence of the ongoing military campaign is a total restructuring of the national budget. The historic “peace dividend” that allowed the state to maintain a stable debt-to-GDP ratio near 60% has entirely disappeared.

- The Sovereign Debt Surge: Driven by immense, unexpected military expenditures, Israel’s public debt-to-GDP ratio has surged to 69%, with total public debt projected to top 70.4% by the end of the fiscal year.

- The Sovereign Bond Squeeze: To fund ongoing multi-theater operations, the government has executed some of its largest bond issuances on record, raising more than $75 billion in 2024 and over $60 billion in 2025, before returning to international markets to secure an additional $6 billion in emergency capital.

- The Fiscal Deficit Expansion: The state’s baseline fiscal deficit is on track to finish above 5% of GDP for the third consecutive year. Emergency budget alterations have been heavily exacerbated by direct confrontations, with the domestic finance ministry confirming that the war has cost the state budget approximately 35 billion shekels ($11.52 billion) in short-term allocations, pushing the targeted deficit deep into a dangerous 4.9% to 5.6% band.

- The Structural Procurement Commitments: Long-term defense planning has shifted completely. Following extended negotiations to balance the national budget, authorities locked in a compromise defense procurement plan worth $94.5 billion over the next 10 years, ensuring that high tax rates, including a value-added tax (VAT) increase to 18%, will remain embedded in the civilian economy for a generation.

III. Sector-by-Sector Attrition Profile

Active Market Performance and Structural Strain Metrics

| Industrial Sector | Primary Vulnerability Vector | Current Operational Status | Long-Term Strategic Outlook |

| High-Technology | Reserve call-ups; international travel risk | Resilient; generated $10.5 billion in mergers and acquisitions | Driven by global demand for battle-proven AI systems and cybersecurity infrastructure. |

| Construction | Absolute exclusion of Palestinian labor pool | Stalled housing starts; building activity down over 40% | Driving domestic home prices back up despite high interest rates. |

| Tourism & Aviation | Ongoing missile alerts; sovereign flight bans | Complete stagnation; international carrier arrivals down 85% | Complete collapse of regional hospitality networks along the periphery lines. |

| Energy & Logistics | Strait of Hormuz blockades; global oil spikes | Domestic gasoline prices rising due to crude pushing past $100 per barrel | Increased reliance on heavily guarded maritime corridors and alternative transit schemes. |

Figure 1: Strategic intelligence matrix charting the multi-year divergence between climbing national debt-to-GDP percentages and contracting domestic consumer spending indexes under the pressure of prolonged reserve mobilizations.

IV. Indicators to Watch

- [MONETARY POLICY] The Central Bank Easing Horizon: Monitor the upcoming interest rate announcements from the Bank of Israel. Following a series of cuts that dropped the benchmark lending rate to 4%, track whether the central bank will be forced to pause its monetary easing cycle to defend the shekel if multi-front defense expenditures push core inflation above the 1% to 3% target band.

- [LABOR MARKET] Per Per-Capita Income Drift: Watch internal workforce allocation updates. With defense spending consuming nearly 8% of total national output, look closely to see if the permanent closure of small businesses in the Galilee and peripheral border zones triggers a long-term drop in net worker productivity, permanently separating per capita GDP from its pre-war growth path.

WarsWW Intelligence Note [REF: SPOTLIGHT-ISRAEL-ECON]

The ultimate lesson of Israel’s current fiscal stress test is that modern, high-tech resilience has an absolute mathematical limit. While the high-tech sector continues to secure foreign venture capital by marketing battle-proven defense innovations, a modern state cannot thrive indefinitely on defense contracts alone. The complete paralysis of the domestic construction sector, combined with multi-billion-dollar business continuity grants and a major surge in national borrowing costs, proves that open-ended multi-front campaigns eventually consume the civilian foundations required to sustain long-term growth. If the regional security environment demands permanent mobilization, the state will have to adjust to a lower baseline standard of living, trading its status as an agile innovation leader for the heavy realities of a permanent fortress economy.